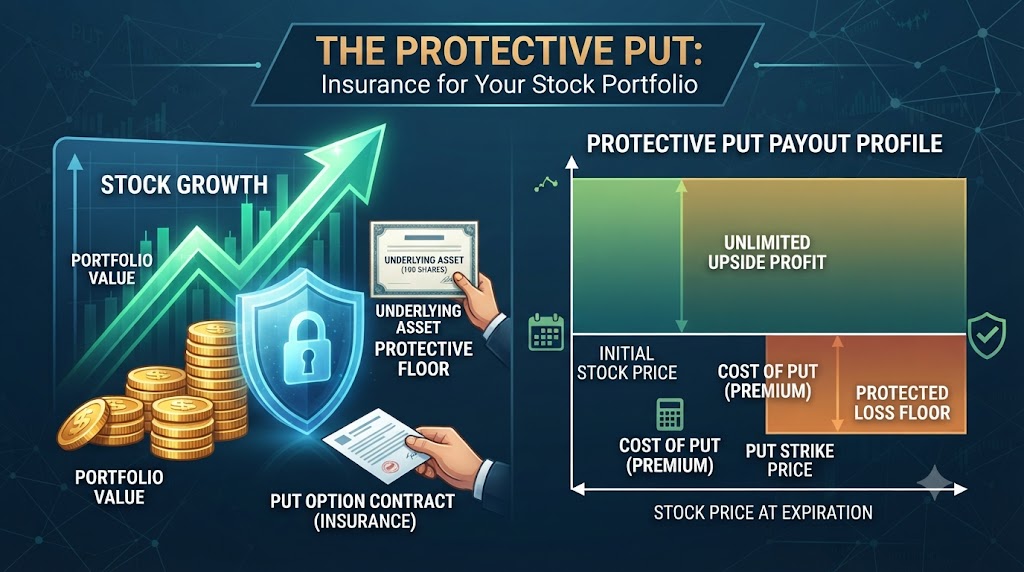

Protective Put to Hedge Your Long Positions

🔍 What Is a Protective Put?

A protective put (sometimes called a “married put” if bought at the exact same time as the stock) involves two components:

- You own 100 shares of a stock (or an ETF like SPY).

- You buy a put option on that exact same stock.

By buying that put, you secure the right to sell your shares at the strike price anytime before expiration, no matter how low the market crashes. You are effectively setting a “price floor” for your holdings.

📊 A Real-World Hedging Example

Let’s say you own 1,000 shares of a tech stock currently trading at $100 per share. You have unrealized gains, but you’re nervous about an upcoming Federal Reserve meeting that could rattle the markets. You don’t want to sell your shares and trigger a capital gains tax bill.

- Your Stock Position: 1,000 shares @ $100 = $100,000.

- The Hedge: You buy 10 put contracts (since each controls 100 shares) with a $95 strike price, expiring in 3 months, for a premium of $2.00 per share ($200 per contract, or $2,000 total).

Here is your financial picture for the next three months:

- Cost of Insurance: $2,000 (this is your maximum loss on the hedge).

- Your “Floor” Price: $95 per share. No matter how far the stock falls, you can sell for $95.

📈 The Two Scenarios at Play

Scenario A (The Market Crashes): Stock drops to $70.

- Your stock portfolio loses $30,000 ($100 to $70).

- Your protective puts kick in. You exercise or sell your puts, allowing you to sell your shares at $95 instead of $70. Your puts gain $25 per share ($2,500 per contract, or $25,000 total).

- Net Result: Your stock lost $30,000, but your puts gained $25,000. Subtract your $2,000 insurance cost, and your total net loss is only **$7,000** (roughly a 7% loss), instead of a catastrophic 30% loss.

Scenario B (The Market Rallies): Stock rises to $115.

- Your stock portfolio gains $15,000.

- Your protective puts expire completely worthless. You lose the $2,000 premium you paid.

- Net Result: You made $13,000 ($15,000 gain – $2,000 cost). You are thrilled, and you simply buy new puts later if you remain nervous.

✅ Why Use a Protective Put for Hedging?

- Unlimited Upside: Unlike a covered call, where you cap your profits, a protective put leaves your upside completely open. If the stock skyrockets, you participate in 100% of the gains (minus the premium you paid).

- Downside Protection: You define your maximum loss. You know exactly how much you can lose, which takes the emotion out of market crashes.

- Tax Efficiency: It allows you to avoid selling your shares. If you have held a stock for years and have capital gains, selling would trigger a tax bill. The protective put lets you “lock in” your current price for a few months without actually selling, deferring those taxes.

- Peace of Mind: It lets you stay invested in the market (which historically trends upward) without lying awake at night worrying about a 20% correction.

⚠️ The Trade-Offs and “Gotchas”

Hedging is not free money. Here are the critical drawbacks you must consider:

- The Cost Drag (Decay): Puts aren’t cheap. If you continuously buy protective puts every quarter, the premiums will act as a constant drag on your portfolio returns. Over a bull market year, this drag could cost you 5%–10% in performance.

- Choosing the Wrong Strike: Buying a put with a strike price too close to the current price (e.g., $98) gives great protection but could be very expensive. Buying a put too far out (e.g., $80) is cheap but only protects you from a total catastrophe.

- Timing is Everything: Options expire. If the crash happens one week after your puts expire, you are left completely unprotected. You have to actively manage and roll your hedges.

💡 Pro Tips for Hedging with Protective Puts

If you decide to use this strategy, don’t just blindly buy puts. Hedge like a professional:

- The “Catastrophe” Hedge (Tail Risk): Instead of buying expensive at-the-money puts (e.g., the $95 strike), buy cheap out-of-the-money puts (e.g., the $85 strike). You won’t profit from a 5% dip, but if the market crashes 15%–20%, these cheap puts will explode in value. It’s like buying disaster insurance.

- Hedge the Index, Not the Stock: If you own a diversified portfolio of 20 different stocks, it’s expensive and messy to buy puts on each one. Instead, buy puts on an index like SPY (S&P 500 ETF) or QQQ (Nasdaq ETF). This hedges your overall market risk (beta) much more cheaply.

- Roll Your Hedges: If your puts are about to expire and the market still hasn’t crashed, you can “roll” them—sell the expiring puts and buy new ones with a later expiration date. This keeps your insurance policy active, though it costs another premium.

- Partial Hedging: Depending on your market outlook and risk aversion, you don’t have to hedge 100% of your portfolio. If you are moderately nervous, hedge only 50% of your holdings. This reduces your cost while still softening a significant blow.

🧠 The Bottom Line

Protective put allows you to remain a long-term, tax-efficient investor while acknowledging that markets don’t go up in a straight line.

While protective put premiums cost money and will eat into your returns during calm years, it allows you to stay calm, hold your ground, and even buy more during a crash, knowing your downside is strictly limited.

To provide high-quality insights, this article was partially or fully written with the assistance of AI technology and reviewed by human contributor.